The dawn of the cryptocurrency era has paved the way for a myriad of opportunities and challenges alike. Among these digital currencies, X11 cryptocurrency holds a significant stature due to its unique hashing algorithm which provides an extra layer of security and energy efficiency. As individuals and businesses venture into the realm of X11 cryptocurrencies, understanding the tax implications becomes an imperative step to ensure compliance with legal norms. This article delves into the tax implications for X11 cryptocurrency holders, shedding light on the taxation rules, capital gains, record-keeping essentials, and strategies to reduce tax liabilities while adhering to the law.

The X11 cryptocurrency, like its counterparts, operates in a decentralized framework, providing a level of anonymity and freedom which is unparalleled in traditional financial systems. However, this decentralization does not absolve holders from the tax obligations in their respective jurisdictions. As governments and tax authorities gradually catch up with the rapid evolution of digital currencies, tax rules are becoming more defined, yet complex.

Importance of understanding tax implications

The importance of understanding these tax implications cannot be overstressed, as failure to comply could lead to severe penalties. Additionally, being well-versed with the tax obligations allows individuals and entities to plan effectively, optimizing their tax positions while staying within the legal confines.

In the subsequent sections, we will unfold the general tax principles applicable to cryptocurrencies, delve deeper into the specifics of capital gains and losses with X11 cryptocurrencies, explore the tax treatment of mining activities, and provide insights on meticulous record-keeping to ensure accurate tax reporting. Moreover, we will touch upon the variations in tax rules across different countries, shedding light on the global landscape of cryptocurrency taxation. Finally, we will discuss legal strategies to potentially reduce tax liabilities for X11 cryptocurrency holders.

What is X11 Cryptocurrency?

X11 is not just another name in the vast sea of cryptocurrencies. It is a unique hashing algorithm that sets itself apart due to its design and functionality. Introduced as a more energy-efficient alternative to the traditional Proof-of-Work systems, X11 comprises a chain of eleven scientific hashing algorithms. This not only offers enhanced security but also provides miners with a cooler and quieter operation.

Key Features of X11

- Multiple Algorithms: X11 uses a sequence of eleven different hashing functions. This makes it more secure as an attacker would need to break all eleven functions, not just one, making attacks considerably more complex and less likely.

- Energy Efficiency: The chained hashing approach ensures that X11 is less resource-intensive, translating to less heat generation and longer hardware lifespan. This is especially appealing for miners who face high energy bills and equipment wear and tear.

- Adaptive Mining: X11 is known for its adaptability, allowing a diverse range of hardware, from CPUs to GPUs and even ASICs, to engage in mining activities.

Basic Tax Principles for Cryptocurrencies

While X11 stands out in the realm of cryptocurrencies, the foundational tax principles that apply to it mirror those of other digital currencies. Here are some fundamental concepts to grasp:

- Property, not Currency: In many jurisdictions, cryptocurrencies like those based on X11 are treated as property for tax purposes. This means that typical capital gains and losses rules apply when they are sold or exchanged.

- Taxable Events: It’s crucial to understand when a taxable event occurs. This could be when you sell your X11-based cryptocurrency for fiat currency, exchange it for another cryptocurrency, or use it for goods and services.

- Fair Market Value: For tax purposes, the value of the cryptocurrency at the time of the transaction is considered. This is termed the ‘Fair Market Value’ and can fluctuate significantly over short periods, making accurate and timely record-keeping essential.

How These Rules Apply to X11 Cryptocurrencies

X11, distinguished by its chain of eleven hashing algorithms, stands out in the crypto landscape. Yet, from a taxation standpoint, its distinctiveness blends into the broader regulatory framework applied to cryptocurrencies at large. Whether evaluating the fiscal implications of mining rewards, accounting for capital gains after a sale, or considering allowable deductions linked to mining expenses, X11 doesn’t deviate from the standard tax norms set for digital currencies. The real challenge for X11 holders stems from its market volatility, necessitating precise transactional records to ascertain fair market value during tax computations. Thus, while X11’s technological nuances are unique, its tax implications largely mirror those established for the greater cryptocurrency ecosystem.

Capital Gains & Losses with X11 Cryptos

Just like any other investment or asset, when you dispose of or use your X11 cryptocurrency, there can be financial gains or losses. These are broadly classified into two categories:

- Short-term Capital Gains: If you hold your X11 cryptocurrency for less than a year (this duration may vary based on jurisdiction) before selling or using it, any profit derived is considered as short-term capital gain. This gain is typically taxed at your regular income tax rate.

- Long-term Capital Gains: If you hold your X11 cryptocurrency for over a year, then the profit from its sale or use is termed as a long-term capital gain. This often benefits from a lower tax rate than short-term gains, providing an incentive for longer-term investment.

How to calculate profits and losses

In the event of a loss, you may be able to offset this against other capital gains or, in some cases, against other types of income. However, the specifics of offsetting and the amount that can be claimed vary across jurisdictions.

Understanding and navigating through the tax landscape of X11 cryptocurrencies can be intricate, but with knowledge and due diligence, it is manageable. In subsequent discussions, we will delve deeper into topics like mining tax implications, the importance of record-keeping, and potential strategies to optimize one’s tax position.

Tax Implications of Mining X11 Cryptocurrencies

Mining, the process of validating and adding transactions to the blockchain, is a crucial aspect of the cryptocurrency ecosystem. For those involved in mining X11 cryptocurrencies, understanding the tax implications is vital.

- Mining as Income: Most jurisdictions treat the cryptocurrency received from mining as income. This means that miners must report the fair market value of the mined coins as income at the time they receive them. Later, when these coins are sold, exchanged, or spent, there’s a potential capital gain or loss involved based on the difference between the initial value and the value at the time of disposition.

- Deductible Expenses: Mining requires substantial computational power and, as a result, significant energy consumption. Equipment costs, electricity, and other associated expenses can often be deducted from the gross mining income, reducing the taxable amount. Depending on the jurisdiction, these might include the depreciation of mining hardware, costs of software or subscriptions, and even part of rent or mortgage if you’re mining from home.

- Mining Pool Fees: Some miners join mining pools to combine computational resources. Any fees associated with these pools might also be deductible. It’s important to maintain detailed records of all these expenses to substantiate deductions during tax filings.

Expenses and Deductions Related to Mining Operations

Engaging in the mining of X11 or any cryptocurrency involves significant operational and capital expenses. Understanding which of these can be deducted can significantly influence a miner’s tax liability. Commonly recognized deductions include:

Hardware and Equipment: The upfront costs for mining rigs, GPUs, and other essential hardware can often be depreciated over several years, depending on jurisdictional tax rules.

Electricity Costs: Mining is energy-intensive. The electricity costs, which often make up a substantial part of a miner’s operational expenses, can typically be deducted.

Software and Subscriptions: Any software or online platform subscriptions that aid in the mining process are often considered deductible.

Maintenance and Repairs: Costs related to the upkeep and repair of equipment can also be considered.

Rental or Lease: If a dedicated space is rented or leased specifically for mining operations, these costs can be accounted for.

It’s crucial to maintain clear records of all these expenses, as they’ll be critical during tax filings and potential audits.

Reporting Mining Income

When a miner successfully mines a new block or earns rewards through a mining pool, this constitutes income. Here’s how one should approach its reporting:

It’s vital for miners to report income based on the cryptocurrency’s fair market value when received, considering potential capital gains or losses for future sales. Depending on the jurisdiction, reporting may be required annually or more frequently. Miners should include both block rewards and transaction fees in their income, account for any mining pool fees, and maintain thorough documentation like screenshots and transaction IDs for verification.

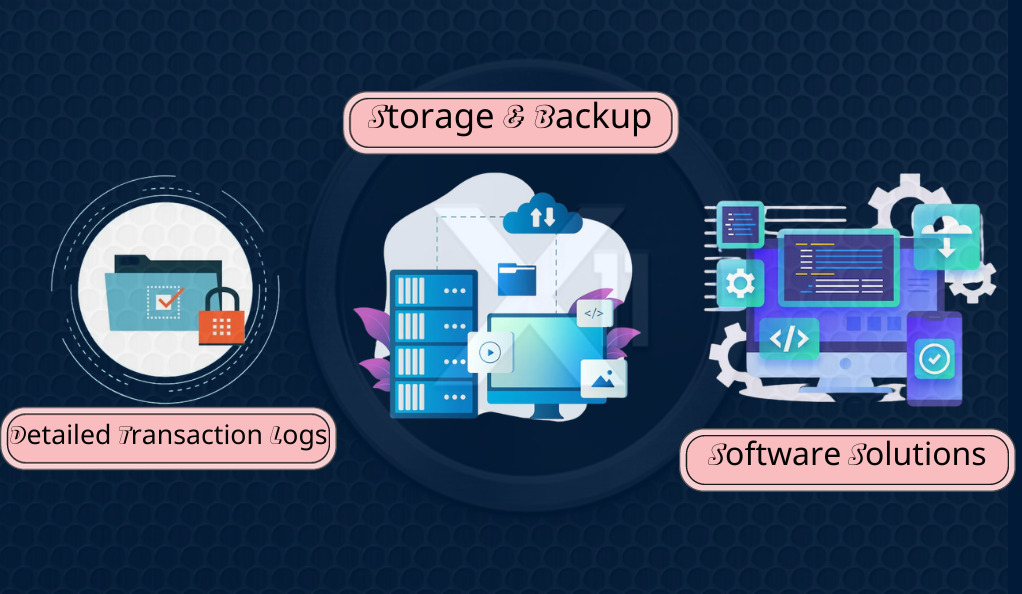

Record-Keeping Essentials for X11 Holders

The dynamic and decentralized nature of cryptocurrencies introduces certain challenges when it comes to tax compliance, chief among them being record-keeping. Here’s what every X11 holder should consider:

- Detailed Transaction Logs: Ensure you have logs of every transaction, no matter how small. This should include date, amount, fair market value at the time of the transaction, and any fees associated.

- Storage & Backup: Given the digital nature of these records, ensure they’re backed up in multiple secure locations. Digital records can be susceptible to loss due to hardware failure, malware, or accidental deletions.

- Software Solutions: Several software tools and platforms have emerged to aid in cryptocurrency tax calculations. They can link to multiple wallets and exchanges, providing a consolidated view of all transactions and helping in estimating tax liabilities.

Taxation Differences by Country

The global nature of cryptocurrencies means that different countries have varying tax rules when it comes to X11 and other digital assets.

- U.S.: The Internal Revenue Service (IRS) treats cryptocurrencies as property. This means capital gains and losses rules apply, and mining is considered self-employment, subject to both income tax and self-employment tax.

- UK: In the UK, Her Majesty’s Revenue and Customs (HMRC) considers individual crypto activities for capital gains tax, while mining activities might be subjected to income tax.

- Canada: The Canada Revenue Agency (CRA) views cryptocurrency transactions as barter transactions, and they could be subject to income or capital gains tax, depending on the circumstances.

- Australia: The Australian Taxation Office (ATO) treats cryptocurrencies similar to assets, subjecting them to capital gains tax.

While the above provides a brief overview, it’s paramount for X11 holders to acquaint themselves with the specifics of their local tax laws or consult a tax professional. This not only ensures compliance but also allows for optimal tax planning.

Reducing Tax Liabilities: Legal Strategies for X11 Holders

Being knowledgeable about your tax obligations is only half the battle. The next step is to devise strategies that help optimize and potentially reduce tax liabilities within the legal framework. Here are some strategies that X11 cryptocurrency holders might consider:

- Tax-advantaged Accounts: Some jurisdictions allow for the purchase of cryptocurrencies within tax-advantaged accounts, such as IRAs or other retirement accounts. When held in these accounts, the capital gains from the sale of the cryptocurrency might be deferred or tax-free, depending on the account type.

- Gifting: Depending on your local regulations, gifting X11 or other cryptocurrencies might not trigger a taxable event. This can be a way to transfer value without immediate tax consequences, though there are often limits to how much can be gifted tax-free annually.

- Charitable Donations: Donating your X11 cryptocurrency to eligible charities might not only provide a tax deduction but also avoid the capital gains tax on the appreciated value.

- Holding Periods: As discussed, long-term capital gains often benefit from a lower tax rate than short-term gains. By holding onto your X11 cryptocurrency for longer durations, you might reduce the overall tax rate applied to any appreciation.

- Harvesting Losses: If you have experienced losses on some of your X11 holdings, selling them can allow you to offset other capital gains. This strategy, known as tax-loss harvesting, can be a way to manage and reduce your tax bill.

- Consider Jurisdiction: For those with the flexibility to do so, considering tax implications might influence decisions about where to reside or conduct business. Some jurisdictions are more favorable for cryptocurrency activities than others.

Conclusion

The world of X11 cryptocurrency boasts a unique algorithm and alluring features. Yet, like all investments, it demands understanding complex tax implications. By maintaining detailed records, understanding local tax rules, and seeking expert advice, X11 holders can remain tax-compliant and potentially optimize their holdings.

With ever-changing cryptocurrency regulations, staying updated is crucial. As tax laws evolve, continuous learning and vigilance are essential for every X11 investor, ensuring informed and strategic investment decisions.

At axerunners.com, our goal is to furnish well-rounded and trustworthy information regarding cryptocurrency, finance, trading, and stocks. Nonetheless, we avoid providing financial advice and instead encourage users to conduct their own research and meticulous verification.

Read More